When a home is damaged by flood, fire, or theft, the policyholder is suddenly asked a very difficult question. What exactly was lost? Can you provide proof of ownership? And do you fully understand what your policy covers?

In theory, this should be straightforward but often is not. One of the biggest challenges in property claims is not the damage itself, but the lack of clear information about what the customer owned and had documented. Many people simply do not have a reliable record of their belongings. When a claim begins, they are asked to recall items from memory while already dealing with the shock and stress of a loss. For many households, documenting belongings after the event can feel almost as stressful and traumatic as the loss itself.

Claims teams see this problem regularly. Insurers and claims assessors often must work with customers to reconstruct information after the loss. That may involve searching for receipts, relying on old photos, or trying to remember details about items that may have been purchased years earlier. What should be a straightforward claim can quickly turn into a slow and frustrating process of reconstruction.

This challenge is becoming more visible as disasters increase. In Australia, insured losses from natural disasters exceeded AUD 2 billion in 2025 according to the Insurance Council of Australia.1 At the same time,

research suggests many households may not have accurate insurance coverage. Some studies estimate that up to 80 percent of Australian homeowners may be underinsured, meaning their policies may not fully cover the replacement cost of their home or contents.2

Why Claims Slow Down

When customers cannot easily confirm ownership or value, claims become more complicated. Adjusters must spend time validating items, confirming categories, and checking whether policy limits apply.

That often leads to several operational challenges for insurers like:

• Longer claims assessment times

• Increased dispute risk

• Higher administrative costs

• Lower customer satisfaction during an already stressful time.

Documentation gaps are also widespread. Surveys suggest that around one in five Australian homes are either uninsured or underinsured, leaving households exposed to financial loss when disasters occur.3

In many situations the issue is not coverage itself. The issue is the absence of reliable documentation about what was owned and what it was worth.

A Shift Toward Preparation

Across the industry there is growing recognition that claims outcomes improve when asset information exists before a loss occurs.

When customers document household items ahead of time, insurers start the claim with clearer information. Ownership is easier to confirm. Policy categories can be understood earlier. Claims can be assessed more quickly and with greater confidence.

Connecting Customer Information with Core Systems

For insurers operating on modern platforms, this shift creates a new opportunity. Structured household data created by customers can support the systems insurers already use to manage policies and claims.

Platforms such as Guidewire provide the operational backbone for many insurers. When customer generated documentation aligns with those systems, insurers gain clearer visibility into household assets before a claim even begins. This supports better claims readiness, clearer coverage conversations, and improved insight across the portfolio.

A New Layer of Preparedness

As insurance operations continue to modernise, preparation before loss will become increasingly important. Technologies that allow customers to document what they own, understand policy limits, and maintain accurate records create a new layer of information that benefits both the insurer and the policyholder.

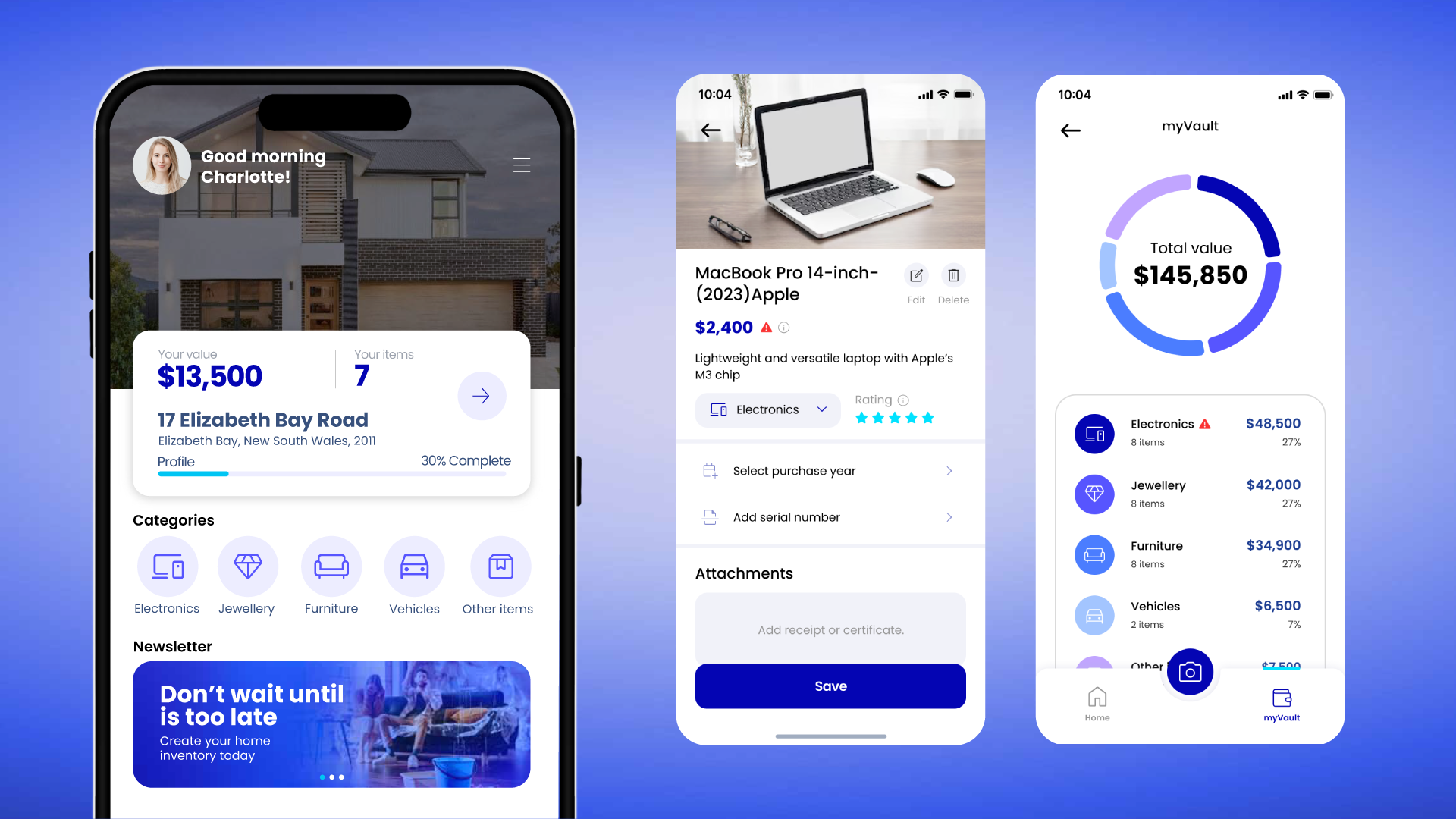

Platforms such as myVal are emerging to support this shift. By allowing homeowners to record photos and videos, with clear descriptions and supporting documents, of their belongings using a smartphone, customers can create a structured digital record of their household assets before a loss occurs. When a claim happens, this information already exists, reducing the need to reconstruct details from memory and helping insurers verify ownership more quickly. In effect, it creates a digital twin of the household, a clear record of what someone owns, supported by documented proof.

For insurers, this improves operational efficiency and claims clarity. For customers, it reduces stress and uncertainty during one of the most difficult moments they may experience.

For the industry, the opportunity is simple. When both sides start a claim with better information, the entire process becomes faster, clearer, and less stressful.

For insurers looking to improve claims efficiency and customer preparedness, the next step is to explore how pre-claim documentation tools can work alongside existing policy and claims systems.

When documentation is in place before a loss, claims move faster and customers can focus on rebuilding their lives.

Source:

1 https://insurancecouncil.com.au/resource/extreme-weather-costs-the-silver-medal-we-dont-want/

Leave a Reply